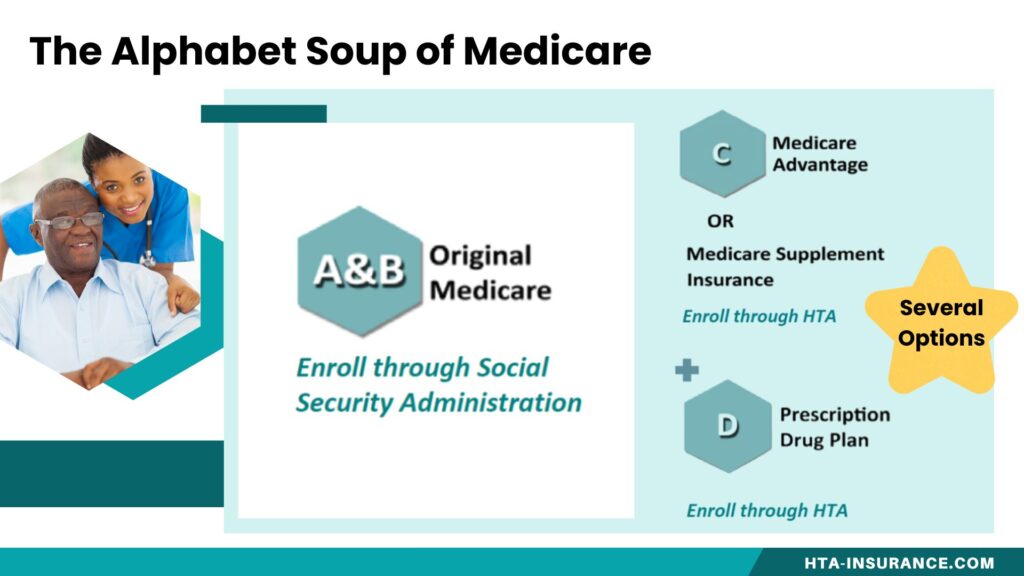

Differences in Plan Types

Medicare Supplement & Medicare Advantage

Medicare Advantage vs. Medicare Supplement: What’s the Difference?

When you enroll in Medicare, one of the biggest decisions you’ll make is how you want to receive your coverage. Most people choose one of two paths: a Medicare Advantage plan or Original Medicare with a Medicare Supplement plan, also called Medigap.

Both options can help with healthcare costs, but they work very differently. The right choice depends on your budget, doctors, prescriptions, travel habits, and how much flexibility you want.

Differences between Medicare Supplement and Medicare Advantage - 6m

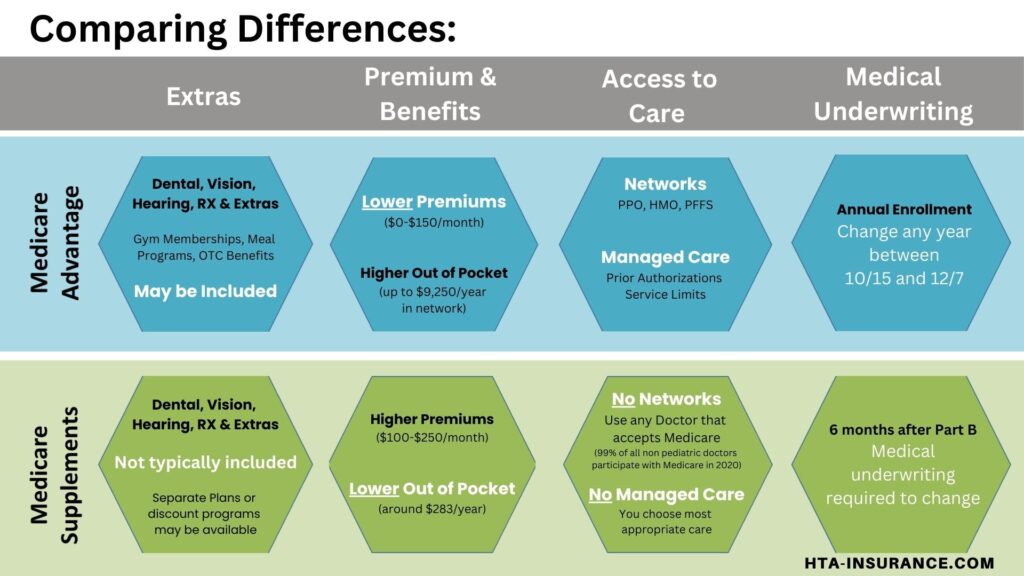

Medicare Advantage: An All-in-One Alternative to Original Medicare

Medicare Advantage, also known as Part C, is offered by private insurance companies approved by Medicare. These plans provide your Medicare Part A and Part B benefits, and many plans also include Part D prescription drug coverage, dental, vision, hearing, fitness benefits, and other extras.

Medicare Advantage plans often have lower monthly premiums, sometimes even $0 premiums, but they typically use provider networks such as HMOs or PPOs. That means your doctors, hospitals, specialists, and pharmacies can matter a lot when choosing a plan. You may also have copays, coinsurance, prior authorizations, referrals, and an annual out-of-pocket maximum for covered medical services.

Medicare Advantage may be a good fit if you:

- Want one plan that combines hospital, medical, and often prescription drug coverage

- Are comfortable using a plan network

- Like the idea of extra benefits such as dental, vision, hearing, or fitness

- Prefer lower monthly premiums

- Are willing to review your plan each year because benefits, networks, costs, and drug coverage can change

Medicare Supplement: Extra Coverage That Works With Original Medicare

Medicare Supplement Insurance, or Medigap, is private insurance that helps pay some of the out-of-pocket costs left behind by Original Medicare, such as deductibles, copays, and coinsurance. To buy a Medigap policy, you generally must have Original Medicare Part A and Part B.

With a Medicare Supplement plan, Original Medicare pays first, and your Supplement plan helps pay its share afterward. These plans generally give you more provider flexibility because you can see any doctor or hospital nationwide that accepts Medicare. However, Medigap plans sold after 2005 do not include prescription drug coverage, so many people pair a Supplement plan with a separate Part D prescription drug plan.

Medicare Supplement may be a good fit if you:

- Want the freedom to see Medicare-accepting doctors across the country

- Travel often or live in more than one state during the year

- Prefer more predictable medical costs

- Do not want to rely on a provider network for most care

- Are comfortable paying a separate monthly premium for the added coverage

")

Medicare Advantage Plans

Medicare Advantage Plans

Medicare Advantage plans, also known as Medicare Part C, are an alternative way to receive your Medicare benefits.

- Medicare Advantage plans work as your primary insurance in place of Original Medicare Parts A and B.

- You must still stay enrolled in Medicare Part A and Part B.

- You are still responsible for paying your Medicare Part B premium.

- These plans are offered through private insurance companies approved by Medicare.

What Medicare Advantage Plans Can Include

Medicare Advantage plans are often considered “all-in-one” plans because they may include additional benefits beyond Original Medicare.

Depending on the plan, benefits may include:

- Medical coverage

- Prescription drug coverage

- Dental benefits

- Vision benefits

- Hearing benefits

- Gym memberships or wellness programs

What Medicare Advantage Plans Must Cover

All Medicare Advantage plans are required to cover the same services covered by Medicare Part A and Part B.

Many plans may also help cover some of the cost-sharing amounts you would normally pay with Original Medicare, such as:

- Copays

- Coinsurance

- Deductibles

Shopping for a Medicare Advantage Plan

All Medicare Advantage plans work differently, so it is important to review the full plan details before enrolling.

When comparing plans, consider:

- What type of network the plan uses, such as HMO or PPO

- Whether your doctors and hospitals accept the plan

- Copays for medical services

- Prescription drug coverage

- Extra benefits, such as dental, vision, hearing, or fitness

- The plan’s maximum out-of-pocket limit

- Whether the plan works well if you travel or live in multiple locations

Re-Evaluating Your Plan

It’s a good idea to review your Medicare coverage each year to make sure it still fits your needs.

Switching to a Medicare Supplement Plan

- Check in with us within your first 6 months on a Medicare Advantage plan.

- This is when you may have the most Medicare Supplement options.

- After 12 months, you may need to answer health questions to qualify.

Changing Medicare Advantage Plans

You can usually change Medicare Advantage plans during:

- Annual Enrollment: October 15 – December 7

- Medicare Advantage Open Enrollment: January 1 – March 31

Medicare Advantage plans are annual contracts, so outside of certain enrollment periods, you may need to wait to make changes.

Can You Have Both?

No. You generally cannot use a Medicare Supplement plan to pay costs from a Medicare Advantage plan. These are two different coverage paths. You typically choose either:

Original Medicare + Medicare Supplement + Part D

or

Medicare Advantage, often with drug coverage included

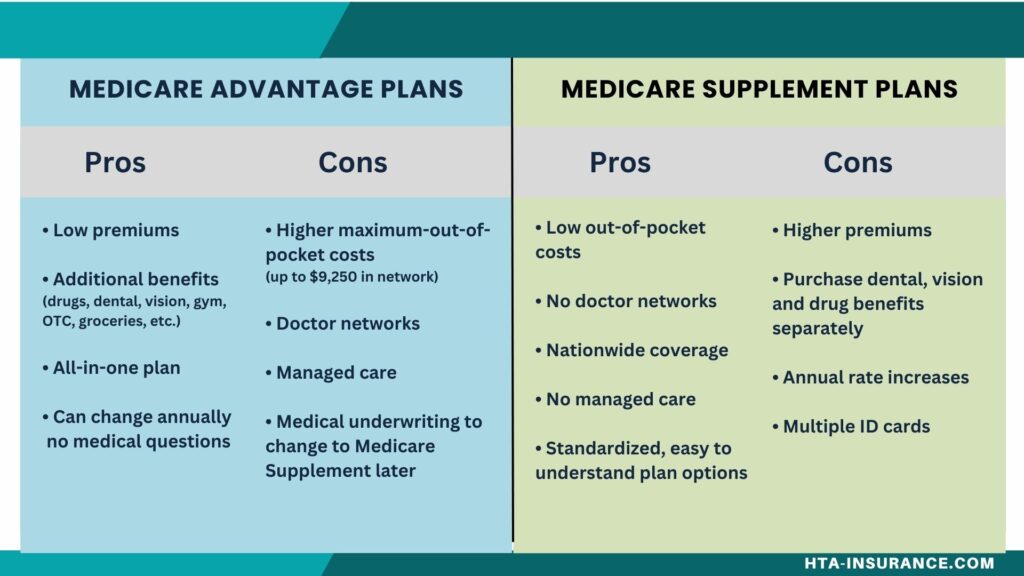

Which Option Is Better?

There is no one-size-fits-all answer. A Medicare Advantage plan may look attractive because of lower premiums and added benefits, but you’ll want to check the network, drug list, copays, prior authorization rules, and annual out-of-pocket exposure. A Medicare Supplement plan may cost more each month, but it can offer broader provider access and more predictable medical expenses.

The best choice depends on how you use healthcare, which doctors you want to keep, what medications you take, and how much financial risk you are comfortable with.

HTA Insurance can help you compare both options side by side so you understand the trade-offs before you enroll.

Why some clients like Medicare Advantage - 2m17s

Why some clients like Medicare Supplement - 1m14s

Medicare Plan Eligibility

To enroll in a Medicare Supplement (Medigap) or Medicare Advantage (Part C) plan, you must first be enrolled in Medicare Part A and Part B.

- Medicare Supplement (Medigap) plans work alongside Original Medicare (Parts A & B) to help cover out-of-pocket costs such as deductibles, copays, and coinsurance.

- Medicare Advantage (Part C) plans provide an alternative way to receive your Medicare benefits, replacing Original Medicare for your medical coverage. However, you must remain enrolled in and continue paying for Medicare Part B.

")

Other Coverages

Extra Benefits: Dental, Vision, Hearing & More

When comparing Medicare Advantage and Medicare Supplement plans, extra benefits may be an important factor.

- Medicare Advantage plans often include dental, vision, hearing, gym memberships, and sometimes a Part B premium giveback. Benefits, networks, copays, and limits vary by plan.

- Medicare Supplement plans help cover Medicare-approved medical costs but usually do not include dental, vision, hearing, or Part B giveback benefits. Some carriers may offer discounts or added perks.

- Standalone dental, vision, and hearing plans are available for those who want separate coverage.

- Routine vision care such as eye exams, glasses, and contacts may require separate vision coverage.

- Medical eye care for conditions such as cataracts, glaucoma, infections, and macular degeneration is typically covered by Medicare.

- Long-term care is generally not covered when it involves everyday personal care, such as bathing, dressing, meal preparation, or transferring.

Home Healthcare, Nursing Home and Assisted Living Coverage

Medicare, Medicare Supplements and Medicare Advantage plans provide limited coverage for Skilled Nursing and very minimal Skilled Home Care. Typically this has to meet extensive criteria including that the care is “skilled”.

This means that if you need help with personal everyday activities like getting dressed, bathing, preparing your meals and/or transferring (getting from a laying to seated or standing position), Medicare will not pay.

It is prudent to have a Short Term Care or Long Term Care plan in place to provide funds to pay for this type of care if you ever need it.

")

Underwriting Considerations

When you first enroll in Medicare Part B, you have a 6-month Medicare Supplement Open Enrollment Period.

During this time, you can choose any Medicare Supplement plan with no health questions and cannot be denied based on your health.

After this period, you may need to answer medical questions, and your options could be more limited.

A few things to know:

- Some states have different rules

- If you lose employer or group coverage, you may qualify for certain plans without medical underwriting

- Medicare Advantage and Part D plans do not require medical underwriting

- You can review or change Medicare Advantage and Part D plans each year from October 15 through December 7

Visit the following pages for more information on plan options

Medicare Supplement Plan Options

Medicare Advantage Plan Options

Medicare Part D Prescription Plans